Revasum: Riding the tailwind of EV, IOT & 5G

Can you capture the revolution in new technologies such as electric vehicles, the roll out of the 5G network or the rise of the internet of things investing in the ASX? Of course.

Revasum manufactures a portfolio of precision solutions that are integral to the manufacturing of semiconductor wafers. The company’s portfolio includes – polishers, grinders and chemical-mechanical planarization (“CMP”) systems for both Silicon and Silicon Carbide (SiC) wafers.

We were introduced to Revasum at the pre-IPO round. So what got us interested in Revasum at this stage? Let’s start with the end market. Revasum’s key end market drivers include:

- Electric vehicles

- The rollout of 5G

- Connected devices and the rise of the Internet of Things (“IoT”)

We believe these are large and growing markets that will require a greater demand for semiconductors for many years. Having exposure to a company with such strong industry tailwinds was a great start to our investment thesis.

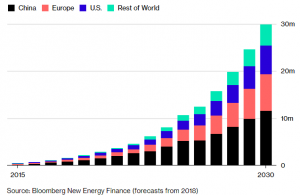

Importantly, Revasum is not exposed to the segments of the market where headline cyclicality concerns are heightened. In fact the segments mentioned above are all entering the start of extended cycles. The chart below from Bloomberg highlights this significant ramp up in electric vehicle sales expectations.

Investing at the pre-IPO stage enabled us to do a great deal of due diligence on the company before its listing on the 6th of December. This included a site tour of Revasum’s head office and manufacturing facility in San Luis Obiso, California.

Having seen the progress versus the pre-IPO forecasts, and with more confidence in the business we also added to our position in the IPO across several funds. We believe Revasum is well positioned to capture the strong industry tailwinds for the following 5 reasons:

- Excellent Management Team

Revasum has a very experienced management team led by Jerry Cutini and Ryan Benton. Jerry and Ryan have over 60years combined experience in the semiconductor and finance industry. Jerry has overseen two successful IPO’s on the NASDAQ and has completed multiple M&A transactions in the semiconductor space. Ryan is currently a non-executive director and Audit Committee Chairman of Pivotal Systems (ASX: PVS). We are attracted to management’s long term commitment to the business. Key management will own 19.1% of the company along with Firsthand Ventures who will own 61.7%. At the IPO there is no sell down and there is a significant escrow period. This highlights the commitment to the success of the business.

- Clear pipeline of products

Revasum has a strong pipeline of future products including, a SiC polishing tool, 200mm CMP system and a 300mm CMP system. The company works closely with its customers on its product initiatives and are developed to meet their needs. As such there is already pent up demand for Revasums next generation products. All these products have a higher average selling price (ASP) than the company’s existing products.

Image: Site tour or Revasum, Pictured in front of their Polisher Machine

- Strong visibility into future earnings

Revasum takes pre-orders on its machines. As per its prospectus the company has over USD21.6m of purchases in hand with a total sales pipeline of USD74.7m post 30 June 2018. Having this higher degree of visibility into future sales gives a greater degree of confidence that Revasum can hit and exceed sales expectations.

- Early mover advantage in SiC

Traditionally semiconductor chips have been built on Silicon wafers. However as technology has advanced Silicon Carbide (SiC) has become more attractive due to its superior physical properties. Whilst adoption of SiC is still early, it is expected to grow rapidly. During my recent trip to the US I managed to spend time with Tesla. Tesla verified the understanding that SiC will be a more popular choice of wafers used in Electric Vehicles. Revasum is one of the leading players in SiC processing and is well positioned to capitalise in the increased market adoption of SiC.

- Underappreciated cost out strategy

Revasum has a well-defined and laid out cost out strategy within the business. Whilst we appreciate the fact that building such complicated machines will always require a need for manual labour, Revasum has identified other input costs that they can reduce. For example on the trip we took to the company’s manufacturing facility we could identify with management their ability to reduce the amount of steel required for the base of the machine. This could reduce the cost by 25%. Along with outsourcing aspects of the manufacturing process we believe there will be a continual improvement in Revasum’s Gross Profit Margin.

This is the view of the author, Ryan Sohn, Equity Analyst at Perennial. The output of his research and analysis can be found in the Perennial Value Smaller Companies Trust and Perennial Value Microcap Opportunities Trust.

This article is general in nature and does not take into account your personal circumstances. Please read the PDS and see our terms and conditions prior to investing.